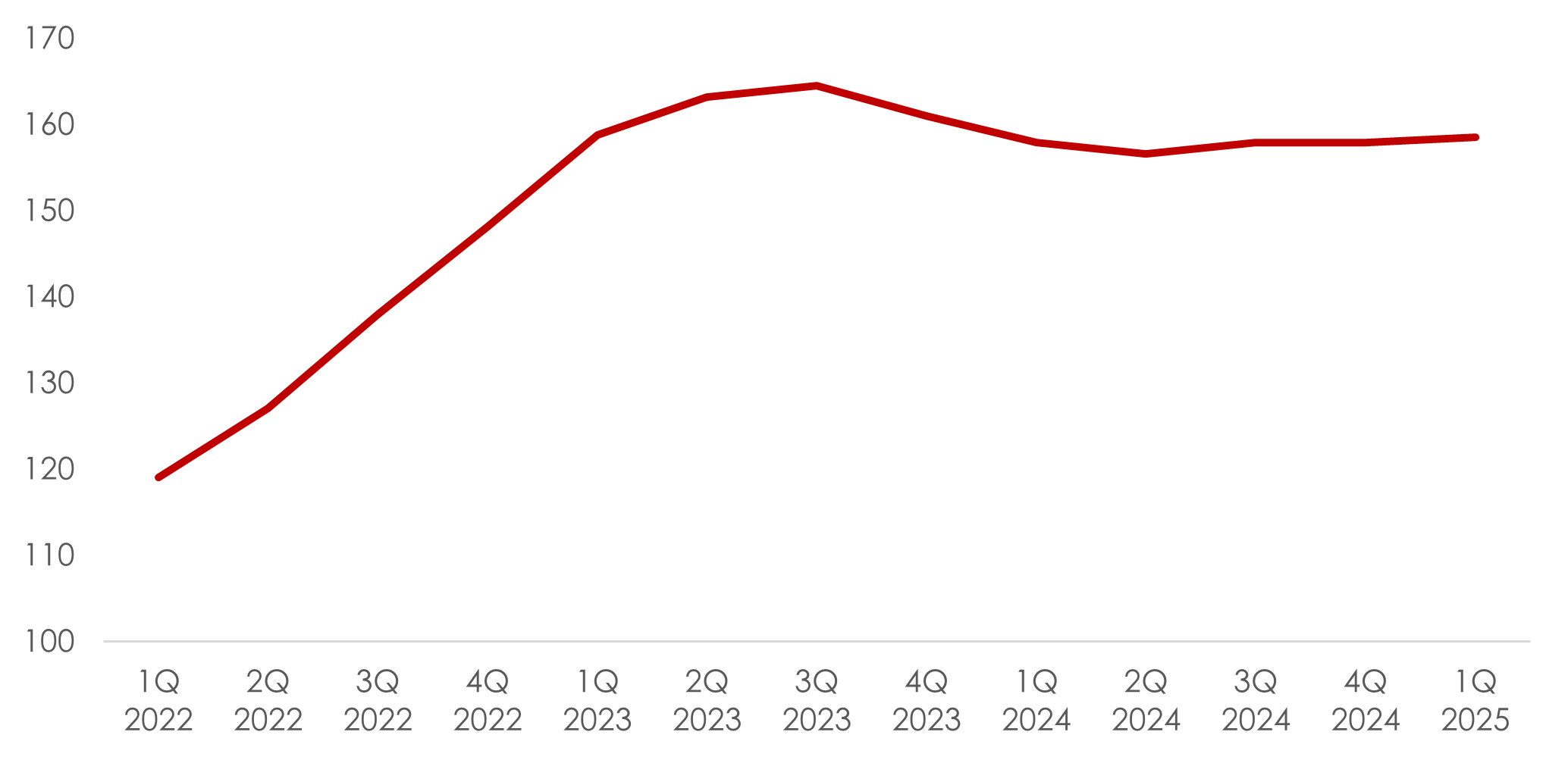

In 1Q 2025, the All-Private Residential property rental index increased slightly to 158.5, marking a 0.4% increase q-o-q and y-o-y. This slight growth follows a period of decline seen previously from 3Q 2023 to 2Q 2024 which saw the rental index drop from 164.5 to 156.6 respectively.

Chart 1: Rental Index of Private Residential Properties

Source: URA as of 28 April 2025, ERA Research and Market Intelligence

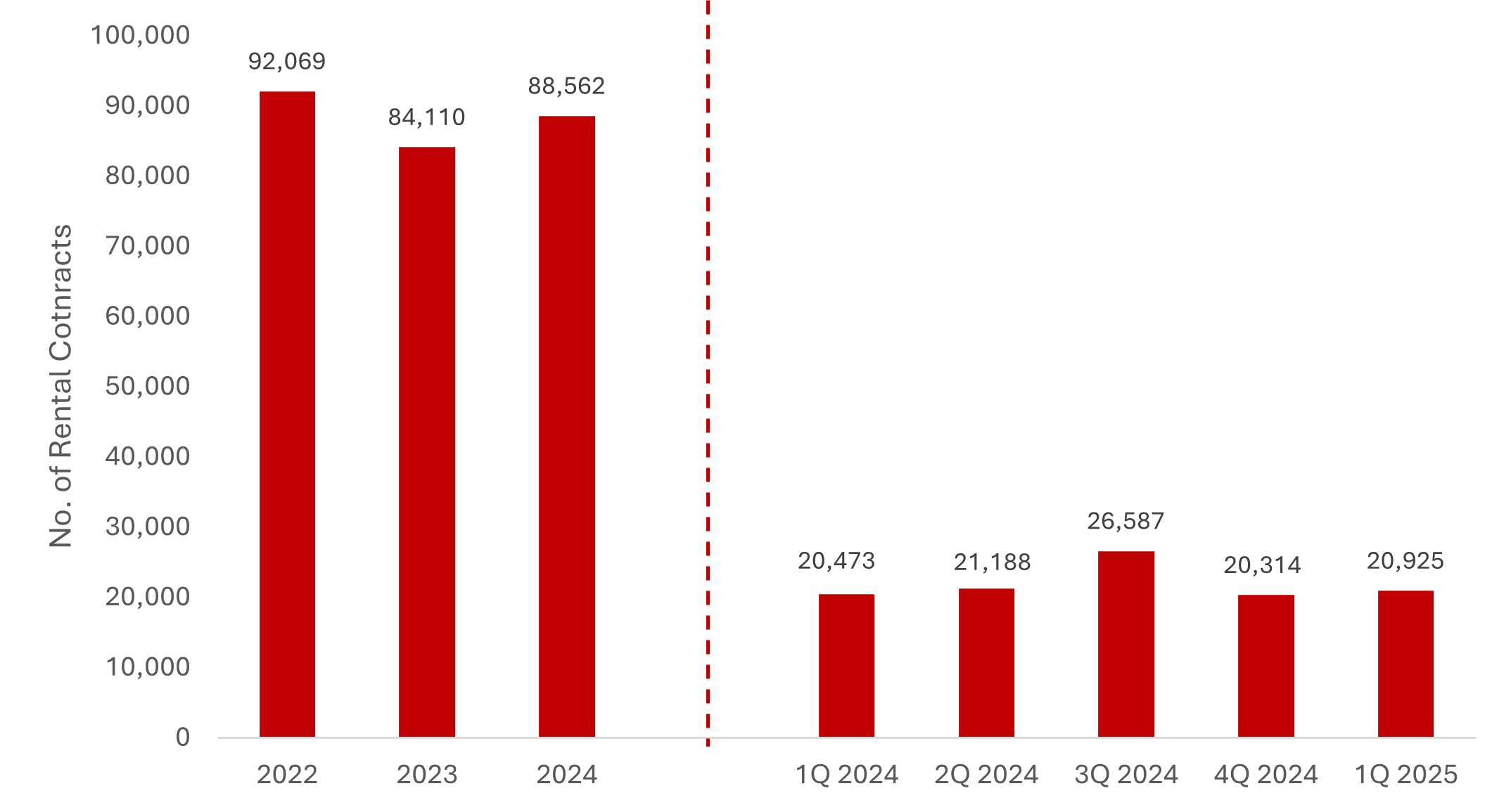

This quarter also saw a total of 20,925 rental contracts for private homes inked, with a 3.0% q-o-q increase and 2.2% y-o-y increase. The increase in rental contracts can be attributed to

Chart 2: Private Residential Rental Contracts

Source: URA as of 28 April 2025, ERA Research and Market Intelligence

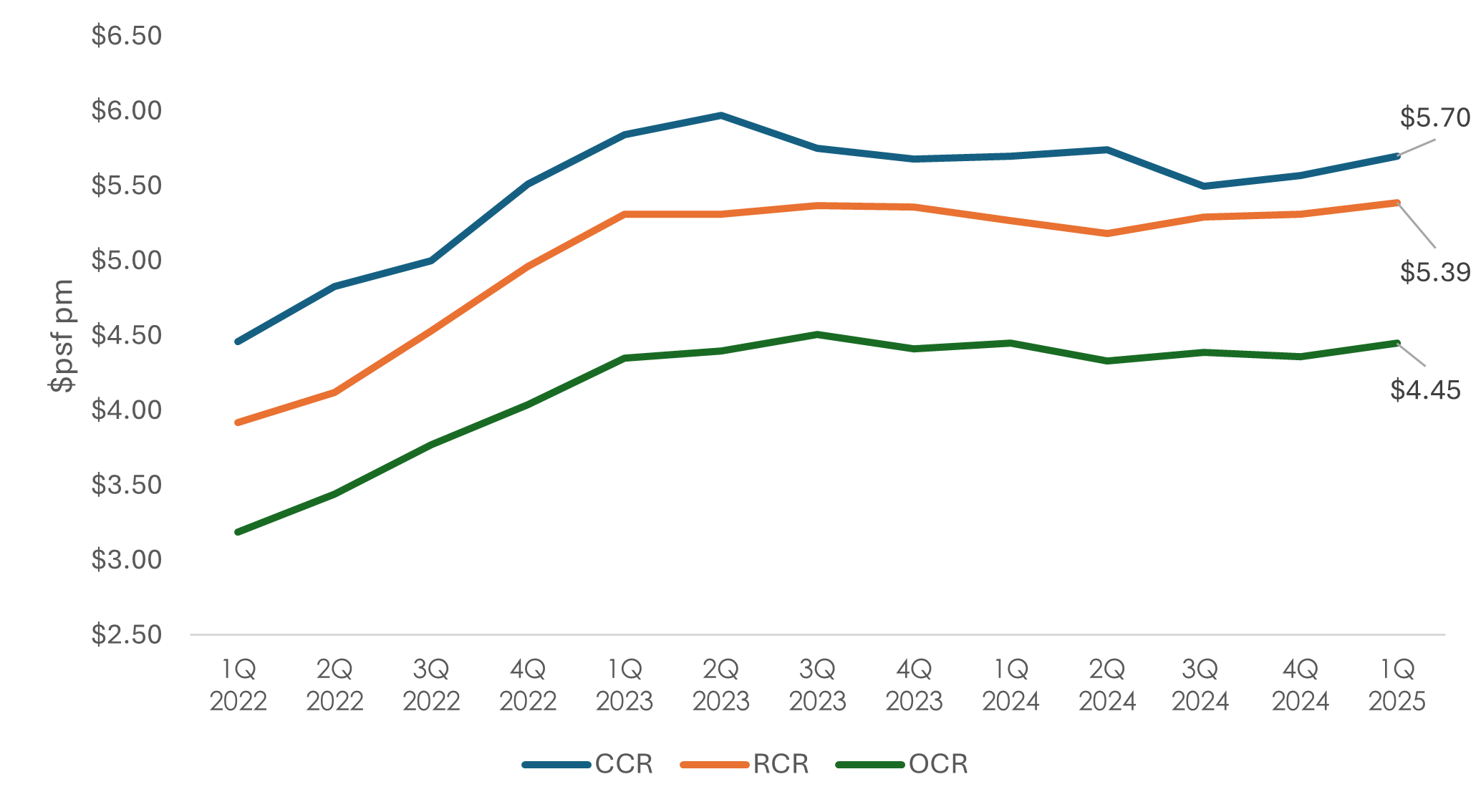

The gradual increase in private home rents stemmed from a lower volume of completions recently. Between 1Q 2024 and 1Q 2025, just 10,291 non-landed private homes attained their Temporary Occupation Period (TOP). This was a drop from 2023, which saw 19,685 non-landed private home completions.

This resulted in upward pressure placed on rents, as the market adjusted to a lack of new supply. Correspondingly, median rents in the Core Central Region (CCR), Rest of Central Region (RCR) and Outside Central Region (OCR) saw upticks of 2.3%, 1.5% and 2.1% q-o-q respectively.

Chart 3: Non-landed median rent by market segment

Source: URA as of 28 April 2025, ERA Research and Market Intelligence

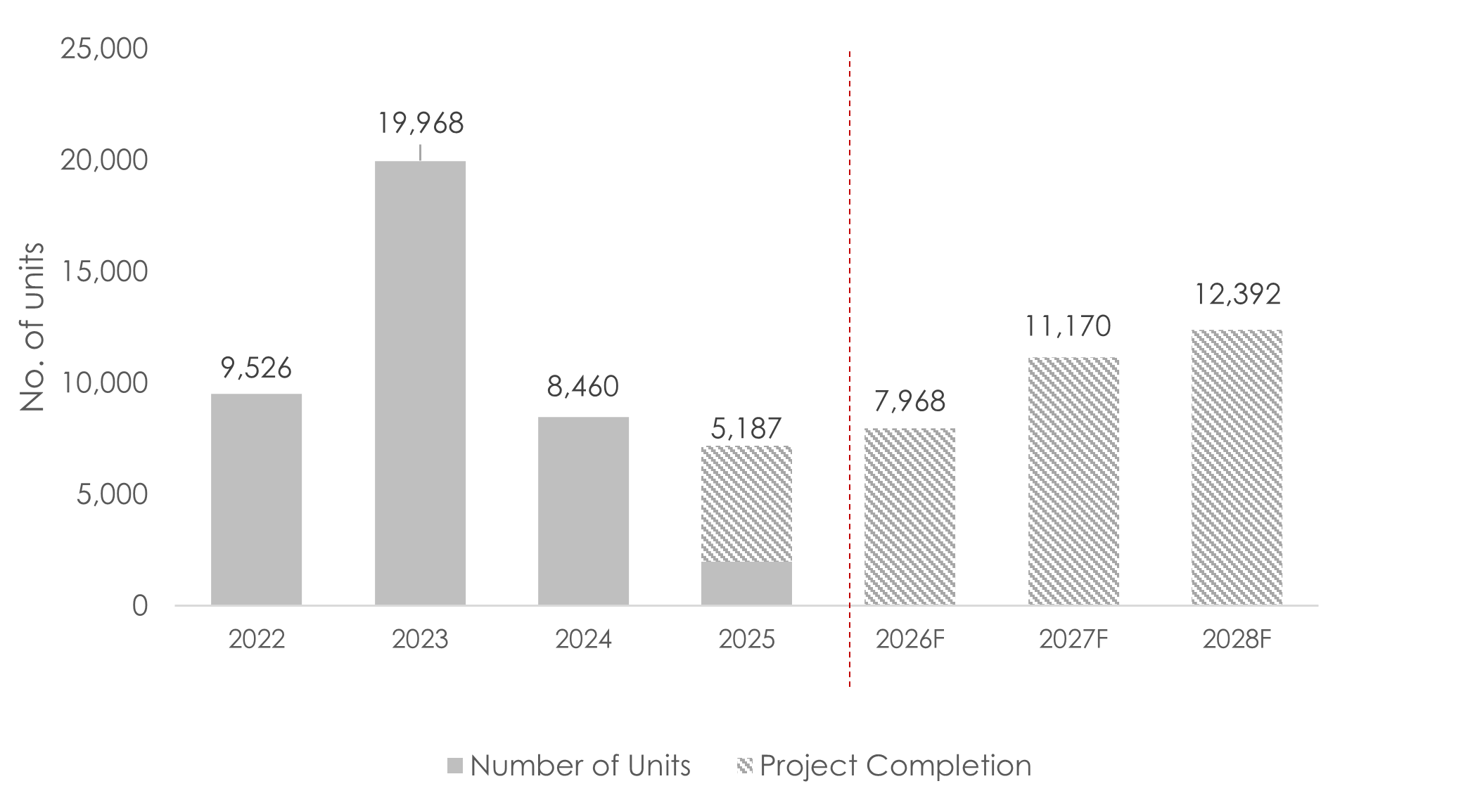

Fall in new private home completions are boosting rental prices

In 1Q 2025, there were 1,988 private home completions. This was a 35.5% drop from 4Q 2024, which saw a total of 3,084 private homes completed. It is expected that new home completions this year will continue to decline with 5,187 units anticipated for the year.

This notable change in supply is expected to drive up rental prices in the coming months, contributing to a slow and steady pace of growth. Landlords of newly completed homes are increasingly seeking higher rental rates, which may support further rental growth in the private residential sector.

Chart 4: Private residential completions

Source: URA as at 28 April 2025, ERA Research and Market Intelligence

Diverging movements in private home rents across market segments

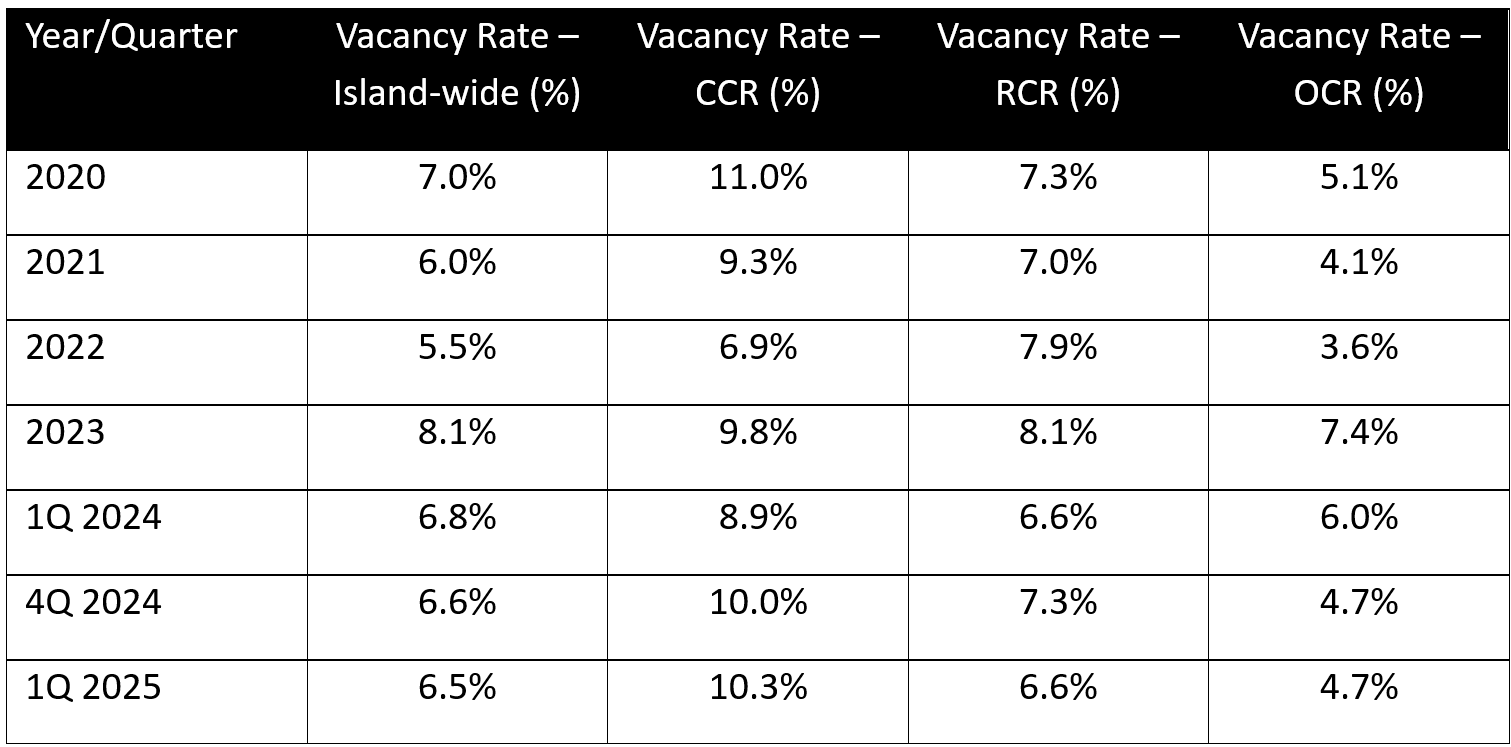

Of the 1,988 completed units in the year, 1,045 units (52.6%) were in the CCR. The vacancy rates of CCR private homes have therefore increased slightly to 10.3% from 10% in 4Q 2024.

Examples include Midtown Modern (558 units) and Pullman Residences (340 units), which contributed to the influx of new units in the market and increased competition for tenants among owners of CCR properties. Newly completed projects like these in prime districts increase the supply of rentable units and place upwards pressure on CCR rents.

Table 1: Historical vacancy rate of completed private residential properties by market segment

Source: URA, ERA Research and Market Intelligence

Conversely, there were only 353 units (18%) completed in the RCR in 1Q 2025, while the OCR accounted for 561 units (28.6%) completed. As the RCR had fewer new units, there were fewer new units for rent. As new units usually command higher rental rates and lifts prices, the RCR median rental saw the smallest growth across all market segments.

Based on these observations, ERA holds a cautiously optimistic view that overall rental prices for private properties will see a marginal increase in 2025, within a projected range of 0% to 3% y-o-y as the market adjusts to the influx of new inventory. We also anticipate the number of private home rental contracts to remain consistent, with numbers expected to reach between 80,000 and 90,000 in 2025.

Median HDB rents increased across all towns in 1Q 2025

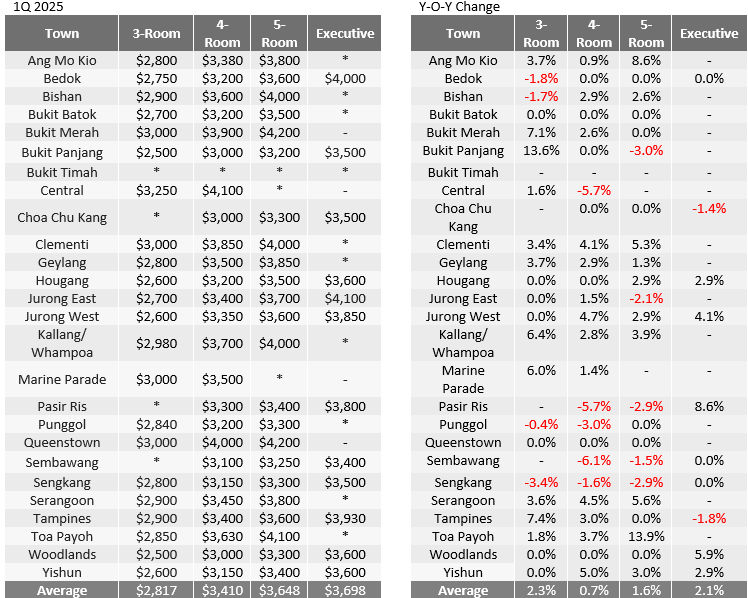

In 1Q 2025, median rents for HDB flats grew across the board for all room sizes. On average, median rents for 3-room and 4-room flats inched up slightly by 2.3% and 0.4% y-o-y respectively. Similarly, modest upticks of 1.6% and 2.1% y-o-y were observed for 5-room and executive flats islandwide over the same period.

Table 2: 1Q 2025 HDB median rents by town and y-o-y growth

(-) Indicates that there are no rental transactions in the quarter

* Indicates that the median rent is not shown because there are less than 20 rental transactions in the quarter for that particular town and flat type

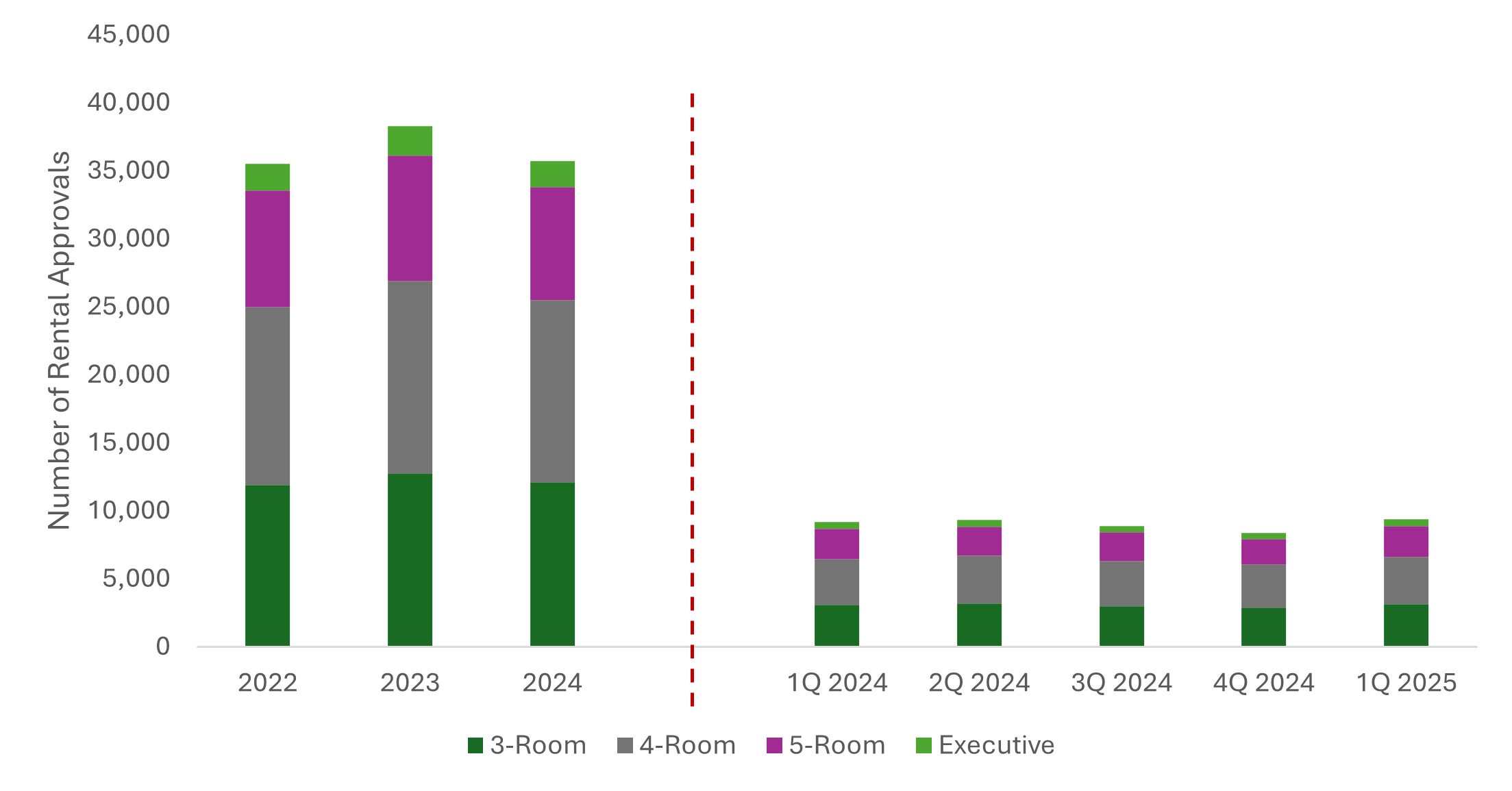

Furthermore, 9,662 HDB flats were rented out in 1Q 2025, representing a 2.8% y-o-y increase compared to 1Q 2024 (9,398 units leased).

Chart 5: Number of rental approvals for HDBs

Source: HDB, ERA Research and Market Intelligence

Price Growth with fewer HDB flats completing Minimum Occupation Period in 2025

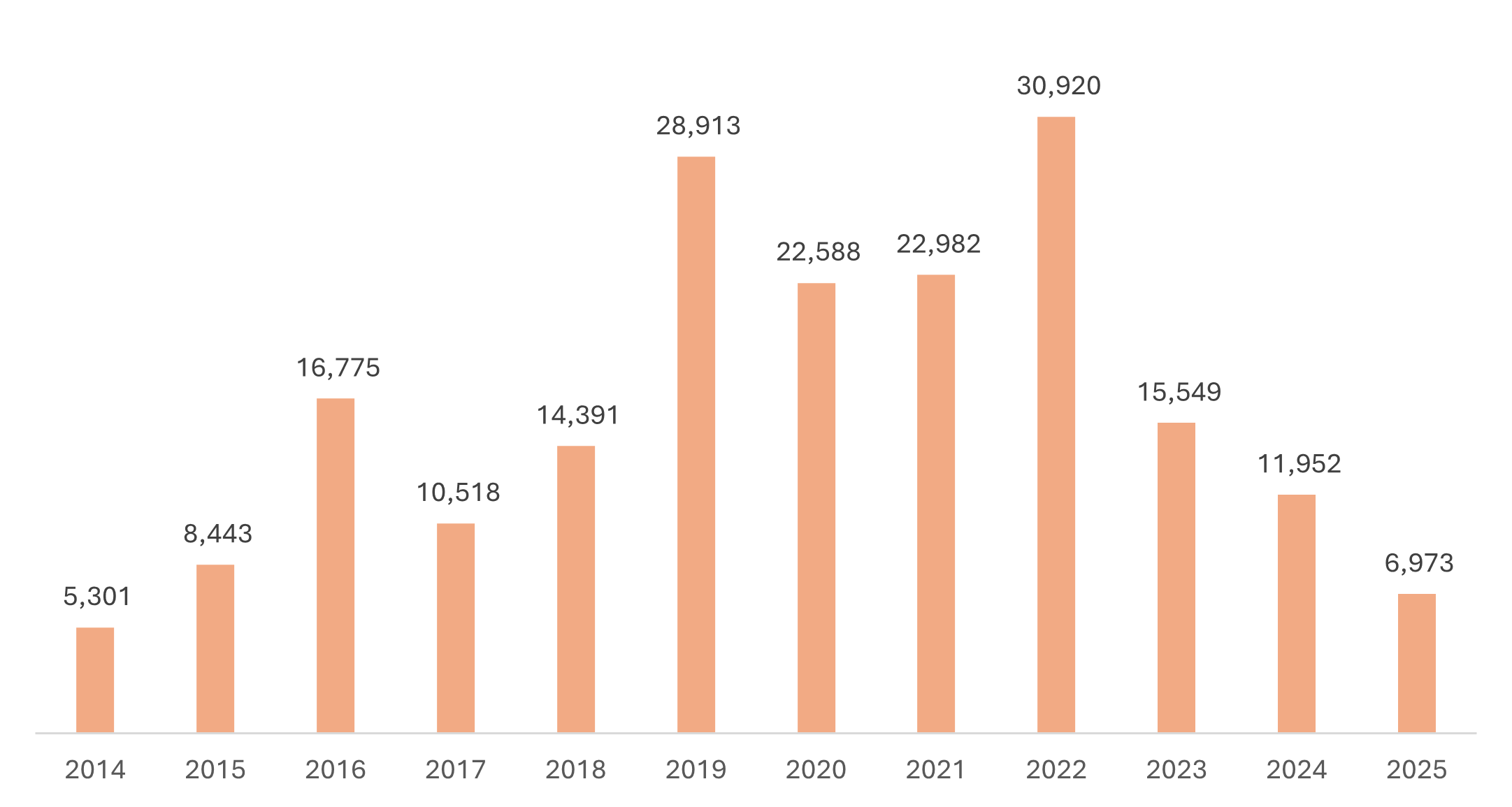

In 2025, an estimated total of 6,973 HDB flats are expected to reach the end of their Minimum Occupation Period (MOP). This is a significant 41.7% decrease from 2024 (11,952 MOP units) and is the fewest MOP flats since 2015, which saw just 8,443 flats attaining MOP. This also marks a continued decline from the peak of 30,920 MOP flats recorded in 2022. The lower overall flat supply has led to increased rental rates.

Chart 6: No. of HDB flats achieving MOP status by year

Source: data.gov.sg, ERA Research and Market Intelligence

Consequently, the HDB leasing market is likely to see prices increasing in 2025 as the supply of MOP flats are low. Factoring in the possibility of a rise in demand for HDB rentals from price-sensitive tenants amid potential economic uncertainty, ERA predicts that HDB rents could rise by 2% to 5% y-o-y this year.

Meanwhile, HDB flat rental volume is expected to range between 34,000 and 36,000 in 2025; this is lower than the full-year estimate of 36,000 to 38,000 for 2024, likewise due to a decrease in the number of MOP flats.

Rental market to favour landlords in 2025 as leasing inventory falls

With the supply of completed units tightening in both the private home and HDB markets, prices in the residential leasing market are primed for growth in 2025. Moreover, assuming no significant changes in economic conditions and foreign worker numbers, rental demand is also likely to stay consistent next year without any significant spikes or declines.

However, rental price growth is likely to diverge across the market, with newly completed homes expected to sustain stronger rent appreciation, while older properties may experience slower to no growth. Similarly, properties in Singapore’s outlying regions could see sharper increases in rents and stronger demand as tenants become more cost-conscious.

ERA forecasts tempered rental price growth for private homes within a projected range of 0 to 3% y-o-y in the face of fewer completions and a more cautious economic outlook. We also anticipate the number of private home rental contracts to remain consistent, with numbers expected to reach between 80,000 and 90,000 this year.

I confirm that I have read theprivacy policyand allow my information to be shared with this agent who may contact me later.