This is part one of an article series examining the Additional Buyer Stamp Duty (ABSD) on foreigners.

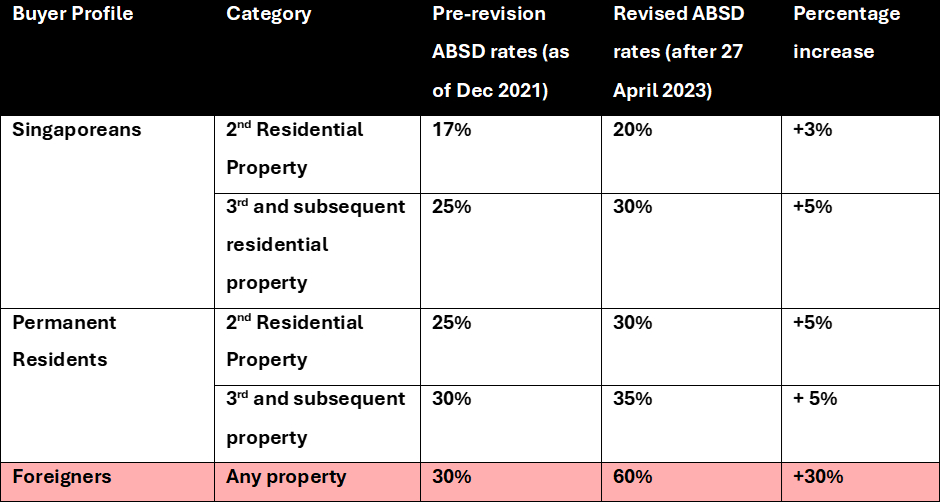

It has been slightly more than two years since April 2023 when the Additional Buyers Stamp Duty (ABSD) was increased across the board. While Singaporeans and Singapore Permanent Residents (SPR) experienced an increase of between 3% and 5% on their second and third property purchases, foreigners faced a much steeper 30% rise, elevating their ABSD rate on any property purchase to 60%.

Hence, with foreigners bearing the brunt of this ABSD adjustment, it calls into question whether the high ABSD rates in the current market environment should be reviewed in the long run.

Introduced in 2011, the ABSD was designed as a cooling measure to curb property speculation and ensure housing affordability amidst strong overseas buying interest in Singapore’s relatively small market. Since then, the ABSD has undergone a series of rate revisions, but its core objective has remained the same: to curb speculation and keep price inflation in check.

Table 1: Timeline of ABSD adjustments

How has the ABSD adjustment impacted demand in the residential market?

Singaporeans have consistently formed the majority of home buyers in the private non-landed residential market (excluding ECs). For instance, between 2Q 2021 and 1Q 2025, local demand from both Singaporeans and Permanent Residents constituted approximately 97% of home buyers island-wide. In contrast, foreigners purchasing Singapore homes accounted for only 3% of transactions over the same period.

Table 2: Share of buyers of non-landed private properties (excl. EC) from 2Q 2021 to 1Q 2025

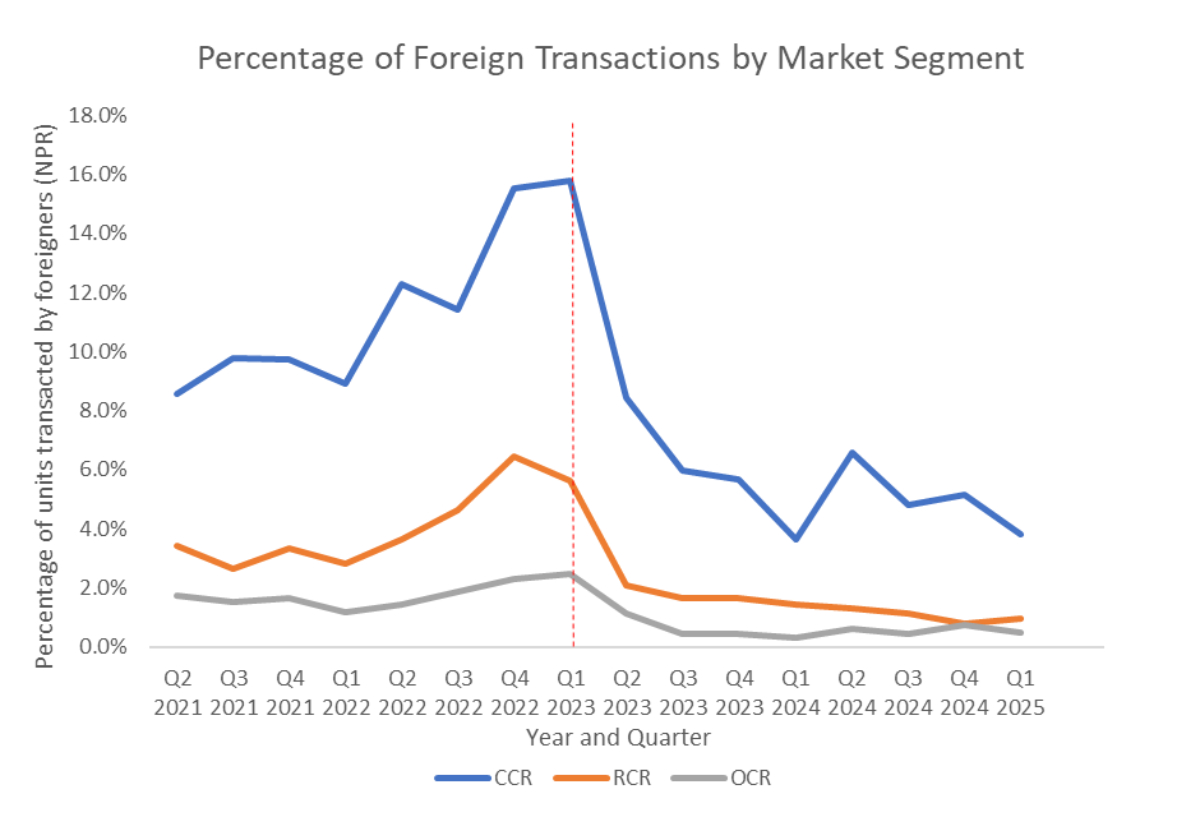

Although foreign demand constitutes a minority, it has traditionally been concentrated in the Core Central Region (CCR) compared to the Rest of Central Region and Outside Central Region (OCR). This is driven by the CCR’s proximity to business hubs and the availability of luxury developments. In 1Q 2023, shortly before the ABSD hike was introduced, the proportion of foreign buyers ranged between 2.5% and 15% across various market segments. Subsequently, the share of foreign buyers declined across all market segments, with the Core Central Region (CCR) being the most affected. The foreign share in the CCR dropped from 15.8% in Q1 2023 to 8.4% in Q2 2023.

Chart 1: Foreign Demand in the Residential Market

Is foreign demand the leading cause of rising property prices?

Consequently, a vital question to consider is whether foreign demand significantly contributes to housing price appreciation. Firstly, we have observed that local demand represented the majority of demand across the CCR, OCR, and RCR, with foreigners making the smallest share of transactions.

While the April 2023 ABSD adjustment effectively curbs foreign demand, it may have a limited effect on reducing price increases in the overall housing market.

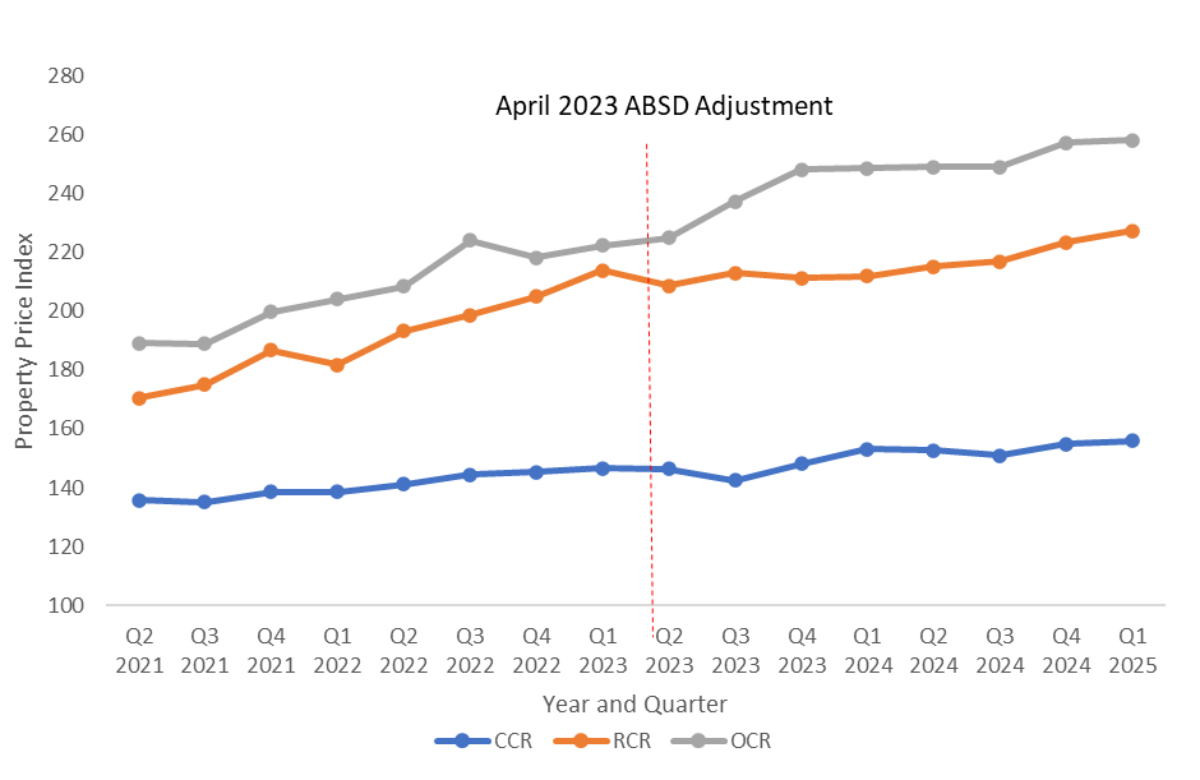

Chart 2: Property Price Index of non-landed private residential properties in CCR, RCR and OCR

Examining the property price index, property price performance for the CCR seems sluggish after April 2023, with a compound annual growth rate (CAGR) of 3.2%, the lowest among the three market segments. Two factors contribute to this. On the demand side, it is evident that the effect of the post-April ABSD adjustment has suppressed foreign demand.

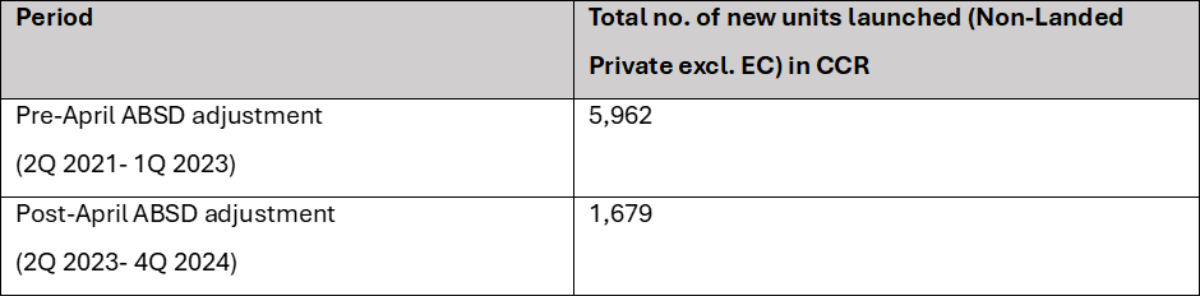

Supply-side factors have also contributed to the slow growth of CCR property prices. As shown in Table 4, there is an overall decrease in new units launched following the ABSD adjustment, which limits the available stock in the CCR and slows down the momentum of price growth. This could also indicate that developers may be more cautious due to the high ABSD rates imposed on foreigners, who represent a significant buyer profile in the CCR.

Table 3: Number of new units launched in the CCR across 1Q 2021 to 4Q 2024

Meanwhile, the RCR and OCR segments have continued to show comparatively more substantial price growth post-ABSD adjustment, sustained by local demand. The continued increase in property prices for RCR and OCR thus demonstrates that local demand remains resilient despite the increased ABSD rates.

Conclusion: Should ABSD rates for foreigners be reviewed?

Local demand has been the primary driver of residential property price growth in Singapore. Despite the sharp increase in ABSD rates, overall prices have continued to rise, further demonstrating foreign buyers' limited impact on prices.

As Singapore continues to position itself as a global business hub, this raises the question of whether it is time to reassess the ABSD rates on property purchases by foreigners in order to preserve the country’s long-term attractiveness. This reassessment should ideally take into account the diverse profiles and intentions of foreign buyers.

In other words, a more nuanced policy approach could be considered – one that distinguishes between speculative investment and genuine housing needs.

On that note, in our next article, we will analyse how the doubling of foreign ABSD rates has affected skilled foreign talent in Singapore and what it signifies for Singapore's future concerning broader policy trade-offs.

I confirm that I have read theprivacy policyand allow my information to be shared with this agent who may contact me later.