Figures are based off the official flash estimates for URA quarterly statistics, released on 1 October 2025.

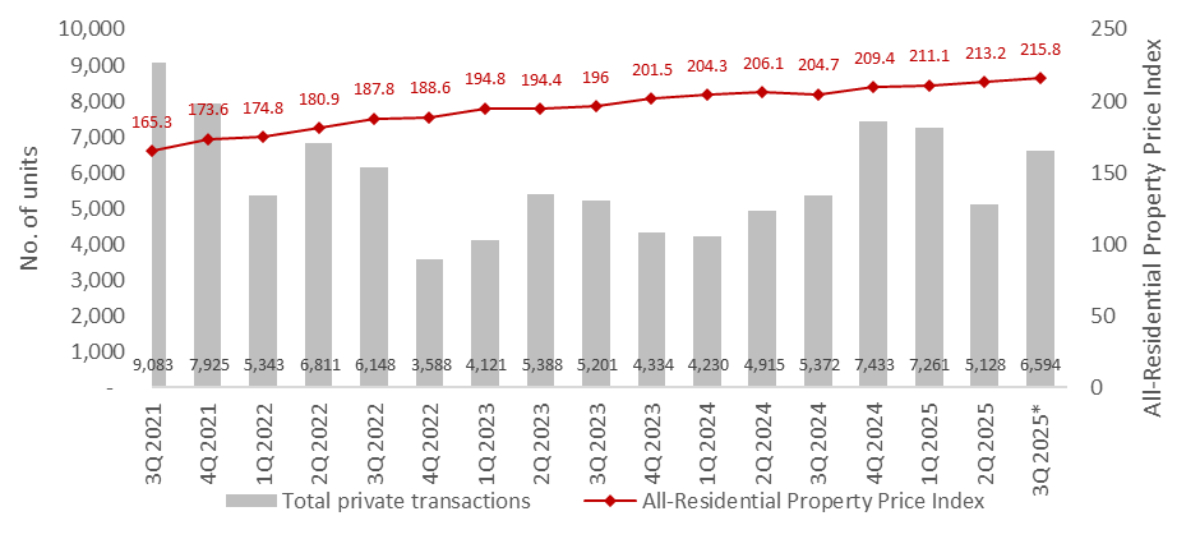

According to flash estimates released by the Urban Redevelopment Authority (URA) for 3Q 2025, the All-Residential Property Price Index exhibited a modest increase of 1.2% quarter-on-quarter (q-o-q), while the total transaction volume of private homes rose 28.6% q-o-q to 6,594 units.

Chart 1: All-Residential Property Price Index and Total Private Transaction Volume

Source: URA, ERA Research and Market Intelligence (*Based on flash estimates)

Source: URA, ERA Research and Market Intelligence (*Based on flash estimates)

The overall non-landed property price index rose 1.1% q-o-q, reaching 209.1 in 3Q 2025. Both private home demand and price growth were boosted by a bumper slate of new launches, concentrated in locations that either experienced a hiatus in fresh supply or saw inaugural launches.

- The Core Central Region (CCR) non-landed price index registered the sharpest increase, reflecting a 2.4% q-o-q uptick due to benchmark pricing at new launches that lifted prices.

- This was followed by the Outside Central Region (OCR), which grew by 1.0% q-o-q, and the Rest of Central Region (RCR), which saw a 0.4% q-o-q increase in corresponding prices.

Meanwhile, the landed property price index rose 1.4% q-o-q, extending last quarter’s uptick. Prices rose amid stronger demand for landed homes from condo upgraders.

In contrast, the secondary market saw a dip in resale and sub-sale transactions over the quarter as buyer focus was redirected to new launches.

New Sale (Non-Landed Homes, Excluding ECs)

According to caveats as at 30 September 2025, new sale transactions saw a rebound by 174.2% q-o-q to 3,238 units in 3Q 2025. This steep increase came on the back of nine new launches in 3Q 2025, yielding a total of 4,154 units.

Based on the current trajectory of new private home sales, 2025 has already surpassed 2024’s full-year tally of 6,469 units, thus underscoring a strong market rebound. Strong new home demand was underpinned by locations that had either experienced a pause in new supply or welcomed their inaugural project.

Chart 2: New Sale Transactions and Median Price for Non-Landed Homes (excluding ECs)

Source: URA as at 30 Sep 2025, ERA Research and Market Intelligence

Source: URA as at 30 Sep 2025, ERA Research and Market Intelligence

In total, nine new launches debuted in 3Q 2025, thus lifting private home prices and transactions. Developers had brought forward some launches ahead of the Hungry Ghost Month in early-September. This also helped to compensate for last quarter’s sluggish performance due to the General Elections and June school holidays.

Table 1: List of new launches in 3Q 2025

Source: URA, ERApro as at 18 Sep 2025, ERA Research and Market Intelligence

Source: URA, ERApro as at 18 Sep 2025, ERA Research and Market Intelligence

CCR Reported Renewed Interest with Four Project Launches

The CCR saw renewed interest this quarter with four launches, UPPERHOUSE at Orchard Boulevard, The Robertson Opus, River Green and the soft-launched W Residences Marina View. This fresh supply contrasts with a subdued year for the CCR in 2024, when only 680 new units were brought to market.

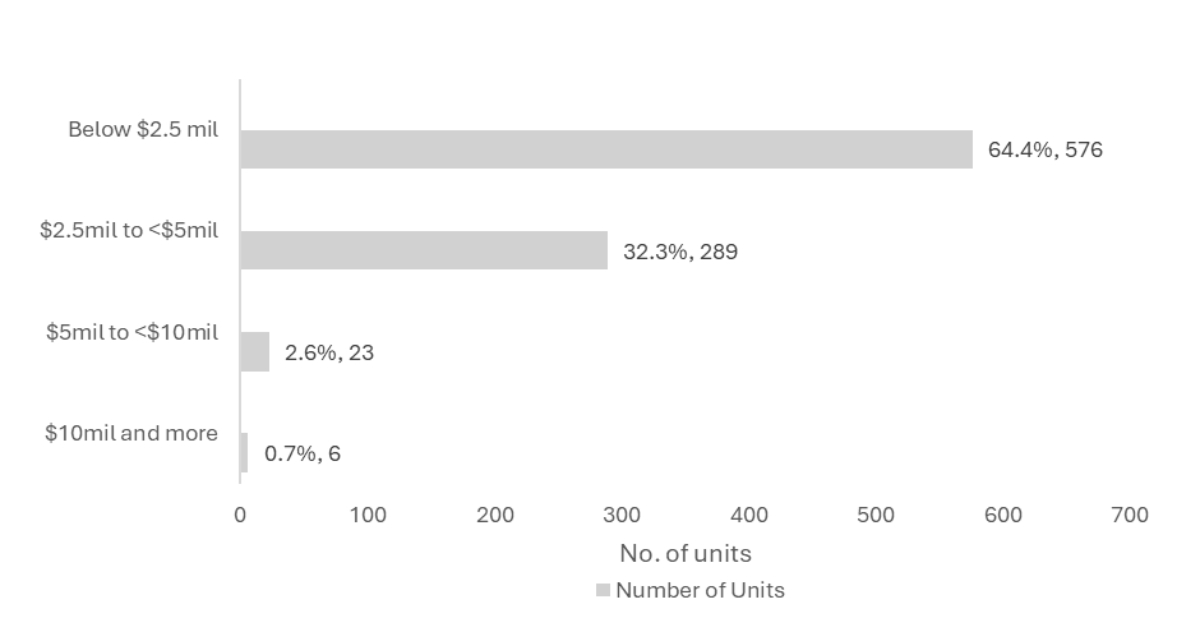

Caveat data (as at 30 Sept 2025) shows that the CCR recorded approximately 894 non-landed private home sales (excluding ECs) in 3Q 2025. This marks the highest quarterly total for the CCR in 15 years since 2Q 2010, when 1,066 units were sold.

Furthermore, nearly two-thirds of CCR new private homes sold in 3Q 2025 were priced below $2.5 million. This ‘sweet spot’ pricing has made the CCR more accessible to local buyers, despite the segment’s traditional positioning as a luxury market.

Buyers were drawn to UPPERHOUSE at Orchard Boulevard’s prime location above Orchard Boulevard MRT. The timely announcement of the 2025 Draft Master Plan for Paterson’s transformation also bodes well for buyers. Similarly, River Green’s attractive price quantum and direct sheltered access to Great World MRT were especially appealing to Singaporean and PR buyers. Meanwhile, The Robertson Opus offers a 999-year tenure, which was keenly pursued by buyers as a legacy asset.

Chart 3: CCR New Sale in 3Q 2025 by price quantum

Source: URA as at 30 Sept 2025, ERA Research and Market Intelligence

Source: URA as at 30 Sept 2025, ERA Research and Market Intelligence

RCR –Science Park and Zion Road Debut Launches saw Positive Take-Up

Lyndenwoods was the best-selling RCR project in 3Q 2025, selling 94.5% of its 343 units during its launch weekend. Its appeal stemmed from being the first residential project in Singapore Science Park, which is set to benefit from the Greater one-north masterplan. The project’s proximity to modern amenities and doorstep access to the Kent Ridge MRT Station further enhanced its attractiveness.

Moving to Zion Road, the launch of Promenade Peak, towering at 63 storeys, appeals to buyers seeking a high-rise development with panoramic views of Singapore’s city skyline. As one of the first launches in the River Valley- Zion Road precinct, the project offers buyers a strong first move advantage.

Lastly, the boutique development, Artisan 8, located along Sin Ming (RCR) has sold over half of its 42 units. It is a freehold development within a 5-minute walk to Upper Thomson MRT Station and a row of eateries. Hence, the allure of a new development in that locale have sparked buying interest, particularly from nearby residents.

OCR –Sales Driven by Pent-Up Demand at Springleaf and Affordable Launch Prices in Canberra

August saw two new launches in the OCR, namely Springleaf Residence and Canberra Crescent Residence. Springleaf Residence is the first high-rise condominium to be launched in the Springleaf housing estate. It sold 884 units (92%) of its 941 units on launch day at a median price of $2,166 psf. Buyers were drawn to its doorstep access to Springleaf MRT Station and lush green spaces, providing a good blend of accessibility and nature. It was also priced attractively, with 64.4% of units priced at under $2 million.

Being Canberra’s first launch in four years, Canberra Crecent Residence benefitted from pent-up demand from residents living in the immediate area. With a median price of $1,993 psf, Canberra Crescent Residence was among the most affordable new launches in the first nine months of 2025.

This quarter also saw previous launches move units, as they were perceived as more attractive buys when compared to newer projects that had set benchmark pricing. Bloomsbury Residences (58 units sold) and One Marina Gardens (40 units sold) stand out for their locations in emerging residential precincts near business hubs. These projects are more investor-centric owing to their location near business hubs and industrial nodes. Hence, as investors take more time to deliberate their options, their take-up rates are more gradual.

In 4Q 2025, five new projects are expected to launch in popular housing estates such as Queenstown, Clementi and Holland, and Zion Road. These projects, Penrith, Skye at Holland, Zyon Grand, The Sens, and Faber Residence, are expected to draw keen buyers’ interest as some of these precincts have not seen new launches in years.

New home sales in the first nine months of 2025 totalled 7,730 units, already surpassing the full-year tally of 6,469 units in 2024. ERA projects full-year sales to come in between 8,500 and 9,500 units, putting 2025 new home sale on track to record the highest since 2021.

Executive Condominium (EC)

In contrast to last quarter, the Executive Condominium (EC) segment saw a sharp spike in transactions, with 569 units sold based on caveat data as of 30 September 2025. This performance is more than twice of the 147 units sold last quarter. The surge was largely driven by the launch of Otto Place at Tengah, where some 559 units have been sold to date, representing 93.2% of its total supply.

Additionally, all existing EC supply have also been fully depleted.

Despite rising prices and a larger down payment required due to the tighter 30% Mortgage Servicing Ratio (MSR) and $16,000 income ceiling, ECs still present value buys in the market when compared to private properties. Unlike private homes, EC remains attractive to HDB upgraders who can benefit from the deferred payment scheme if required and are not subject to the ABSD.

Additionally, Otto Place is within a short walk to two upcoming MRT stations, Tengah Park and Bukit Batok West on the Jurong Region Line.

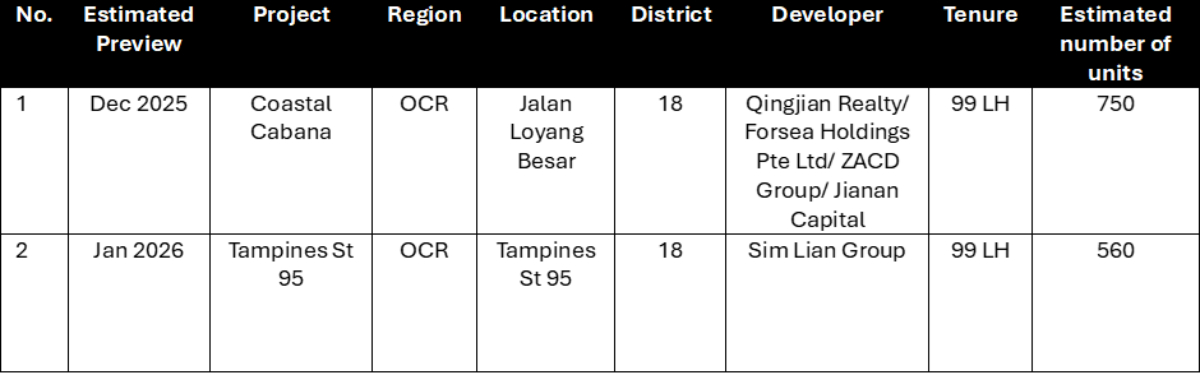

Following this, buyers can look toward to the launch of the 748-unit Coastal Cabana at Jalan Loyang Besar in January 2026. The site was awarded to Qingjian Realty in August 2024 at $729 psf ppr.

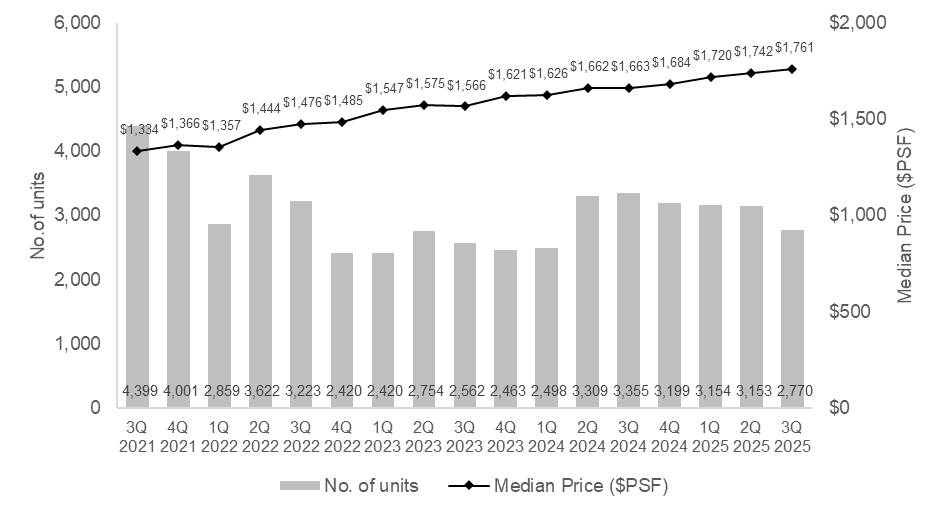

Resale and Sub-Sale (Non-Landed Homes, Excluding EC)

In 3Q 2025, resale transactions for non-landed private homes (excluding ECs) fell 12.5% q-o-q to 2,762 units. This also represents a break in the steady pattern of resale transaction volumes, which has held steady around the 3,000-unit mark for the last five quarters.

The diversion of buyer attention away from the resale market was primarily due to the bumper supply of new home launches in attractive locations, which offered fresh opportunities and more choices.

Chart 4: Resale Transactions and Median Price for Non-Landed Homes (excluding ECs)

Source: URA as at 30 Sept 2025, ERA Research and Market Intelligence

Source: URA as at 30 Sept 2025, ERA Research and Market Intelligence

In contrast to the downtick in transaction volume, median unit prices for resale non-landed private properties (excluding ECs) rose 1.1% q-o-q to $1,761 psf in 3Q 2025. This measured rise reflects stable growth in the segment. It also continues the upward momentum observed since 4Q 2023.

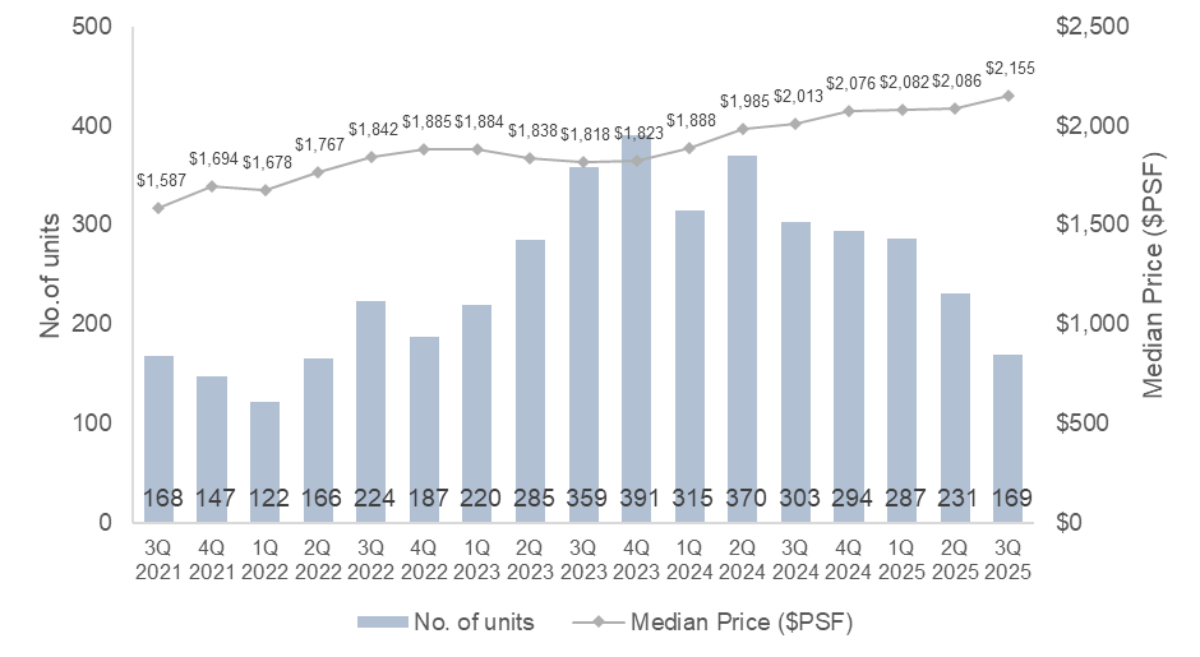

Chart 5: Sub-Sale Transactions and Median Price for Non-Landed Homes (excluding ECs)

Source: URA as at 30 Sept 2025, ERA Research and Market Intelligence

Source: URA as at 30 Sept 2025, ERA Research and Market Intelligence

Within the sub-sale segment, transaction volumes fell 26.8% q-o-q to 169 deals based on caveat data. This translates to sub-sales accounting for 2.7% of all non-landed private property (excluding ECs) deals made in 3Q 2025.

Full-year private home completions (excluding ECs) are projected to reach 4,949 units by end-2025, down from 8,460 units in 2024. This decline is the primary factor behind falling sub-sale transactions, which have been on a steady downward trend since 2Q 2024.

On the other hand, the median unit price for sub-sales rose 3.3% q-o-q to $2,155 psf. This uptick likely resulted from a higher proportion of sub-sale transactions in the CCR (18 units) and RCR (81 ). Together, transactions in the CCR and RCR made up 62% of all sub-sale activity for 3Q 2025, while the OCR accounted for a smaller share of 38% (60 units), based on caveat data as of 19 September 2025.

Aligning with this trend, RCR developments like Normanton Park (27 units) and Penrose (19 units) saw the greatest number of sub-sales during the quarter.

Market Outlook

Recent upgrade of the GDP growth forecast for 2025 from 0–2% to 1.5–2.5% for the whole of 2025, had helped lift consumer sentiment, underpinning strong homebuyer demand in 3Q 2025.

Separately, the introduction of new housing neighbourhoods in areas such as Dover, Defu, Newton and Paterson, in addition to integrated community hubs in Sengkang, Woodlands North, and Yio Chu Kang on top of other initiatives. Together, these developments could help promote buyer confidence by reinforcing the Government's long-term plans for urban renewal and liveability.

In 3Q 2025, some nine new private home launches (totalling 4,154 units) across various estates in Singapore, catering to a diverse range of buyer needs. In particular, the CCR is set to see four new launches in 3Q 2025, following a relatively quiet pipeline in recent years. Come 4Q 2025, sales momentum is set to continue with five new launches slated to add another 2,578 units.

Within the secondary market, it is expected that resale and sub-sale transactions will continue to moderate as a shrinking number of fresh completions continues to weigh on available supply. Additionally, the robust pipeline of upcoming projects has correspondingly diverted buyer demand from the resale and sub-sale markets.

Looking ahead, ERA projects new home sales to fall between 8,500 - 9,500 units for the whole of 2025. In conjunction, sub-sale and resale transactions are also expected to reach between 1,100 to 1,300 units and 14,000 to 15,000 units respectively by the close of 2025.

Table 2: Upcoming launches in 4Q 2025 and 1Q 2026

Executive Condominium

Source: ERA Project Marketing

Source: ERA Project Marketing

I confirm that I have read theprivacy policyand allow my information to be shared with this agent who may contact me later.