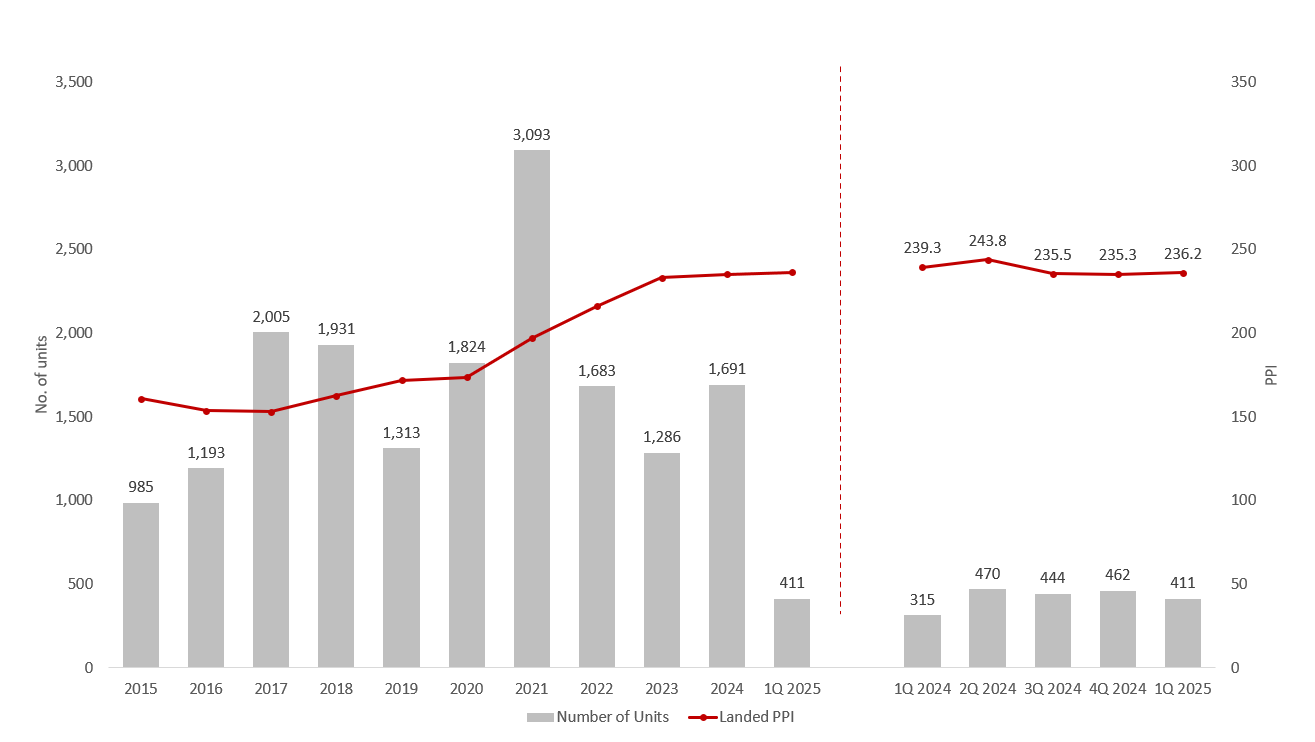

The Landed Price Index rose 0.4% quarter-on-quarter (q-o-q) in 1Q 2025, reversing the 0.1% decrease seen in 4Q 2024. This occurred despite fewer landed homes being transacted in 1Q 2025.

Landed Property Price Index and Transactions

The Landed Property Price Index remained largely stable in 1Q 2025, reporting a growth of 0.4% q-o-q. However, this was still a 1.3% decline year-on-year (y-o-y).

Meanwhile, landed property transactions declined by 11.0% quarter-on-quarter but increased by 9.6% compared to last year.

The increase in landed transactions compared to a year ago could be largely due to the moderating interest rate environment and rising non-landed home prices, which have paved the way for Singaporeans to upgrade to landed homes.

Chart 1: Landed Property Price Index and Transactions

Source: URA as of 26 Apr 2025, ERA Research and Market Intelligence

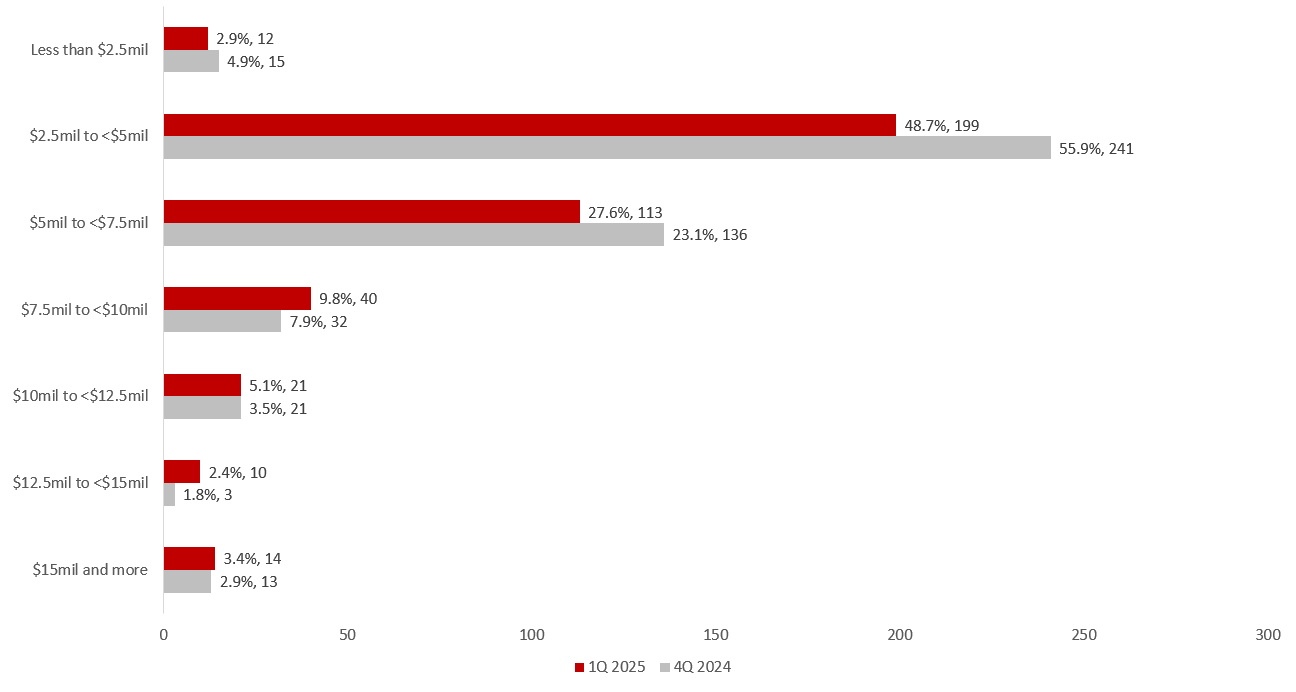

Price Quantum

Under half of the landed homes sold in 1Q 2025 were priced below $5 million. Meanwhile, the $5 million to $10 million segment experienced a 0.8% contraction in sales volume, while the sub-$5 million segment saw a more significant 17.6% quarter-on-quarter decrease in transactions.

In contrast, demand for high-end landed homes grew in 1Q 2025, with URA caveats indicating a 21.6% quarter-on-quarter increase in transactions for landed properties valued at $10 million and above.

The highest-priced deal in 1Q 2025 was a Good Class Bungalow (GCB) located at 21 Gallop Park. This 16,307-square-foot freehold home was reportedly sold by Chua Soon Hock, the founder of Singapore hedge fund Asia Genesis Asset Management, for $58 million. Another GCB at 16A Leedon Park was sold for $45.8 million.

Due to Singapore’s political and economic stability, particularly during this period of uncertainty, GCBs, characterised by their consistently strong demand and limited supply, are viewed as safe haven assets that offer a hedge for long-term wealth preservation and will continue to attract newly minted Ultra-High Net Worth citizens.

Chart 2: Price Quantum 4Q 2024 versus 1Q 2025

Source: URA, ERA Research and Market Intelligence

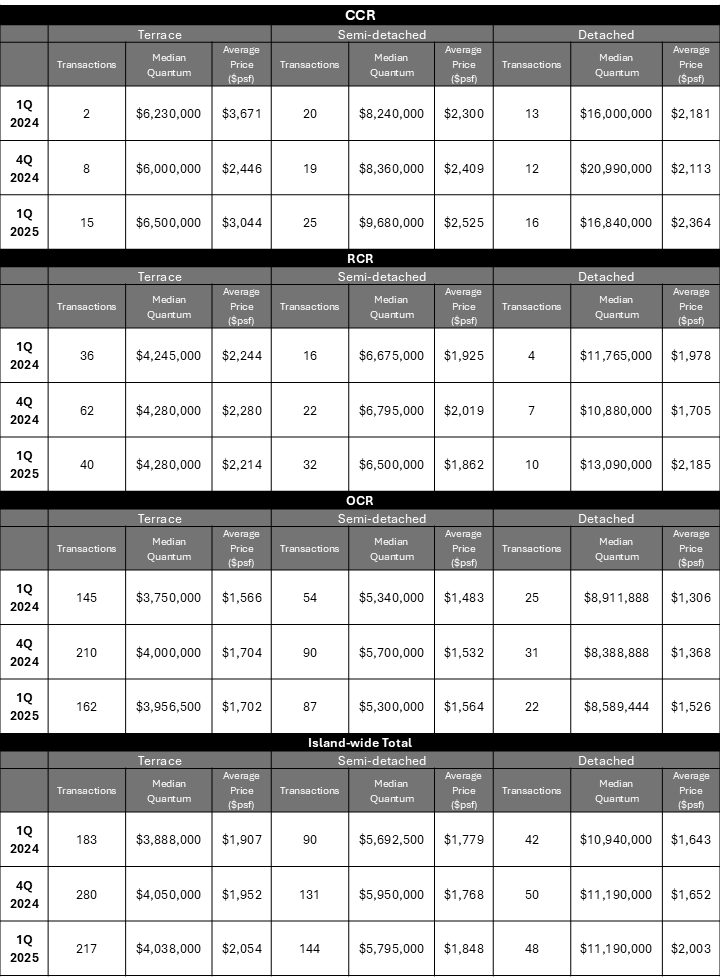

Type of properties

Overall, the number of semi-detached and detached homes sold remained similar to 4Q 2024. However, fewer terrace homes were sold in 1Q 2025 (217 units) compared to the 280 units in 4Q 2024.

Outside the Core Central Region (CCR), terrace houses experienced a sharp decline in transaction volume, mainly due to high prices. Nonetheless, demand for larger homes remained strong, with semi-detached homes recording a 31.6% quarter-on-quarter increase and detached homes seeing a 33.3% quarter-on-quarter increase, respectively.

Table 1: Transaction Volume and Average Price by Landed Property Type/Market Segment

Source: URA as of 17 Apr 2025, ERA Research and Market Intelligence

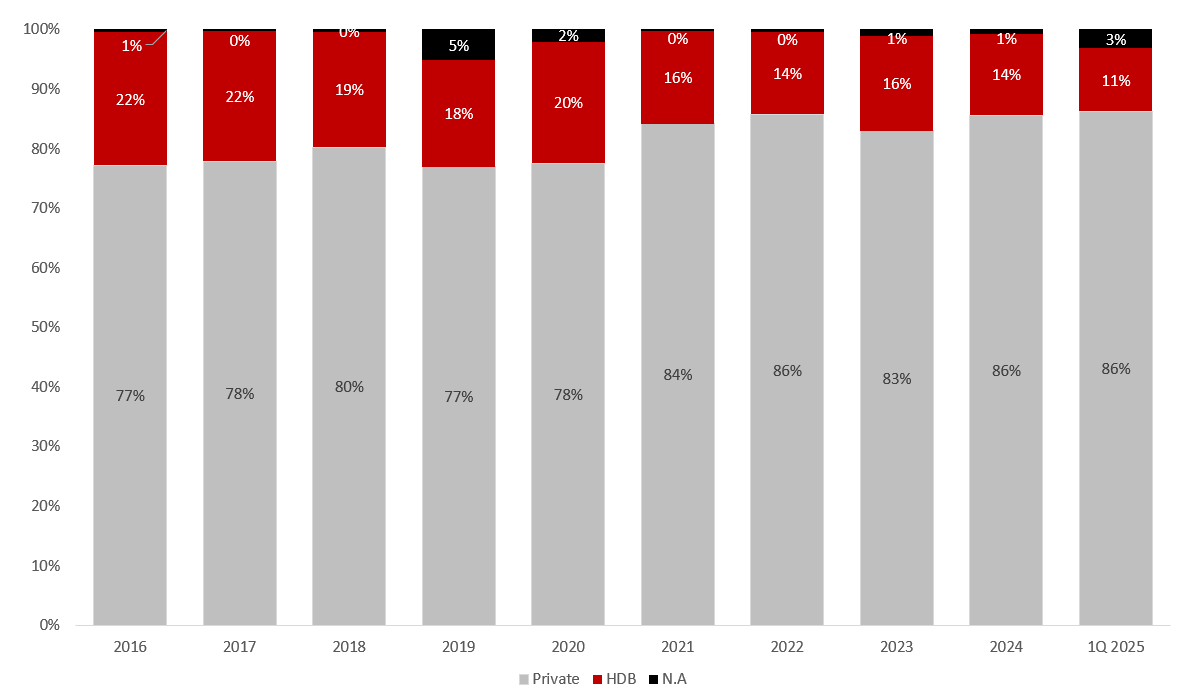

Purchasers address indicator

Amid rising landed housing prices, the proportion of HDB owners upgrading to landed properties continues to shrink further in 1Q 2025. While landed upgraders with HDB addresses represented 14% of the total upgrader population in 2024, that percentage decreased to 11% in 1Q 2025. Although HDB resale prices have risen for the 23rd consecutive quarter, upgrading to landed homes remains more challenging due to their significantly higher starting prices.

This finding also aligns with a trend that began in 2017, specifically a steadily shrinking share of HDB-to-landed upgraders from the last high of 22% in that year.

Chart 3: Landed home buyer profile

Source: URA, ERA Research and Market Intelligence

In conclusion

With potentially strong economic headwinds and geopolitical uncertainties, upgraders may not be willing to pursue landed homes in the short term. Moreover, rising prices and elevated-for-longer interest rates could price some buyers out of the landed home market.

On the other hand, larger landed homes with a higher price quantum could still experience strong demand. Wealthier buyers with greater purchasing power may view this as an opportune time to enter the market, especially given the limited supply of such homes.

With landed homes experiencing a slight decrease in transactions in 1Q 2025 and facing ongoing economic headwinds, ERA has revised its earlier forecast to a year-on-year price growth of 3-5%. Taking into account only non-strata landed homes. we estimate between1,500 to 1,800 landed transactions for 2025.

I confirm that I have read theprivacy policyand allow my information to be shared with this agent who may contact me later.